Introduction

Understanding asset depreciation is essential for accurate financial reporting and tax planning. One of the most effective accelerated depreciation methods is the double declining depreciation formula. This method allows businesses to depreciate assets faster in the early years of their useful life.

In this guide by The Daily Business, we’ll break down the double declining depreciation formula, how it works, and when to use it.

What Is the Double Declining Depreciation Formula?

The double declining depreciation formula is an accelerated depreciation method that applies a higher depreciation rate to an asset’s book value each year.

Unlike straight-line depreciation, which spreads costs evenly, this method front-loads depreciation expenses—meaning higher expenses in the early years and lower expenses later.

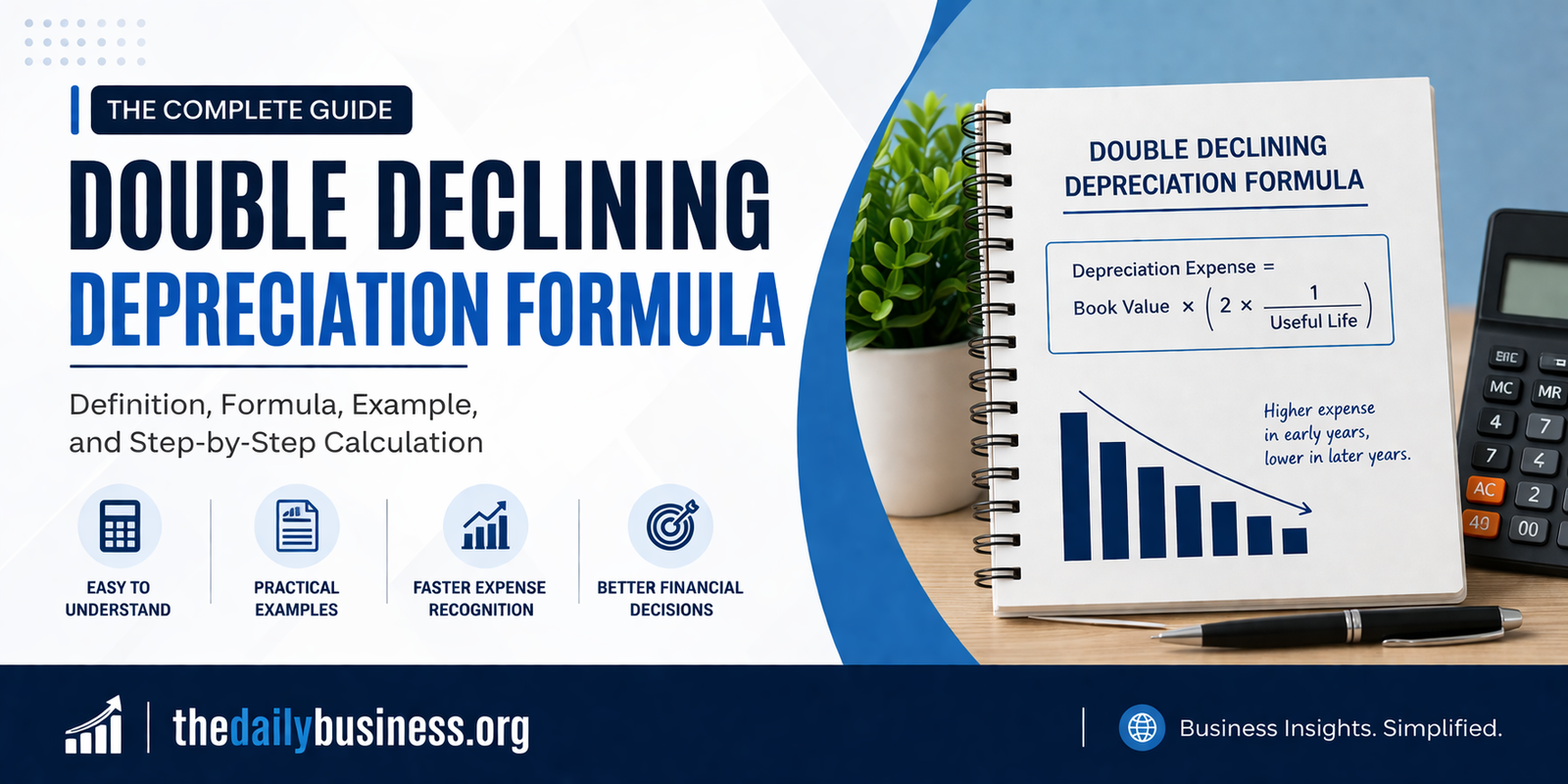

Double Declining Depreciation Formula

The formula is:

Depreciation Expense = Book Value at Beginning of Year × (2 ÷ Useful Life)

Where:

- Book Value = Asset cost minus accumulated depreciation

- Useful Life = Estimated lifespan of the asset

- 2 ÷ Useful Life = Double the straight-line depreciation rate

Step-by-Step Calculation Example

Let’s say a company purchases equipment for $10,000 with a useful life of 5 years.

Step 1: Calculate Straight-Line Rate

1 ÷ 5 = 20%

Step 2: Double the Rate

20% × 2 = 40%

Step 3: Apply the Formula

- Year 1:

$10,000 × 40% = $4,000

Book Value = $6,000 - Year 2:

$6,000 × 40% = $2,400

Book Value = $3,600 - Year 3:

$3,600 × 40% = $1,440

And so on, until the asset reaches its salvage value.

Key Features of the Double Declining Depreciation Formula

1. Accelerated Depreciation

Expenses are higher in the early years, reducing taxable income sooner.

2. No Salvage Value in Initial Calculation

Salvage value is considered at the end, not during yearly calculations.

3. Declining Book Value

Depreciation is always applied to the remaining book value, not the original cost.

Advantages

- Improves cash flow in early years

- Matches higher productivity of new assets

- Reduces taxable income faster

- Useful for technology and equipment assets

Disadvantages

- More complex than straight-line method

- Lower profits reported in early years

- Not suitable for all asset types

When Should Businesses Use It?

The double declining depreciation formula is ideal when:

- Assets lose value quickly (e.g., machinery, electronics)

- Maintenance costs increase over time

- Businesses want early tax advantages

Double Declining vs Straight-Line Depreciation

| Feature | Double Declining | Straight-Line |

|---|---|---|

| Expense Pattern | Higher early | Even yearly |

| Complexity | Moderate | Simple |

| Tax Impact | Faster deductions | Gradual |

| Best For | Rapidly aging assets | Long-term assets |

Common Mistakes to Avoid

- Ignoring salvage value at the end

- Applying the rate to original cost instead of book value

- Using the method for assets that don’t lose value quickly

Conclusion

The double declining depreciation formula is a powerful accounting tool that helps businesses accelerate depreciation and improve early cash flow. While it requires careful calculation, its benefits make it a popular choice for companies managing high-value assets.

For more business finance insights, stay connected with The Daily Business—your trusted source for practical and professional guidance.