Introduction

Depreciation is a crucial concept in accounting that helps businesses allocate the cost of assets over time. One of the most effective accelerated depreciation techniques is the double declining balance method calculation. This method allows businesses to record higher depreciation expenses in the early years of an asset’s life, which can be beneficial for tax planning and financial reporting.

In this guide by The Daily Business, we’ll break down the concept, formula, step-by-step calculation, and real-world examples to help you fully understand how it works.

What Is the Double Declining Balance Method?

The double declining balance (DDB) method is an accelerated depreciation method. Unlike the straight-line method, which spreads the cost evenly, DDB applies a higher depreciation rate in the earlier years.

This approach reflects the reality that many assets—like machinery or vehicles—lose value more quickly when they are new.

Formula for Double Declining Balance Method Calculation

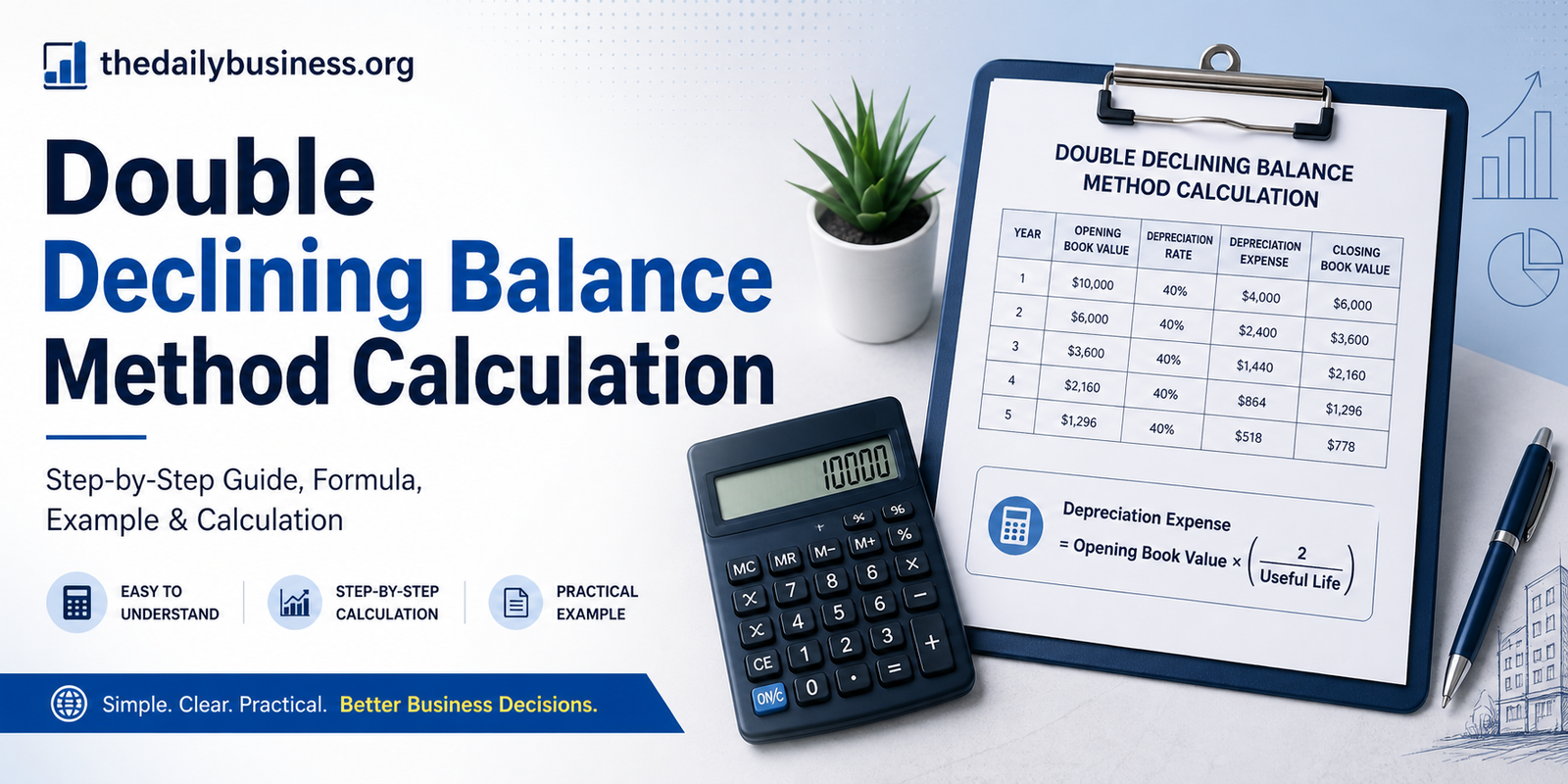

The formula is simple:

Depreciation Expense = Book Value at Beginning of Year × (2 ÷ Useful Life)

Where:

- Book Value = Cost of asset – accumulated depreciation

- Useful Life = Estimated lifespan of the asset

- 2 ÷ Useful Life = Double the straight-line depreciation rate

Step-by-Step Calculation

Let’s understand the double declining balance method calculation with an example:

Example:

- Asset Cost = $10,000

- Useful Life = 5 years

- Salvage Value = $1,000

Step 1: Calculate Straight-Line Rate

Straight-line rate = 1 ÷ 5 = 20%

Step 2: Double the Rate

DDB rate = 20% × 2 = 40%

Step 3: Apply Depreciation Each Year

| Year | Beginning Value | Depreciation (40%) | Ending Value |

|---|---|---|---|

| 1 | $10,000 | $4,000 | $6,000 |

| 2 | $6,000 | $2,400 | $3,600 |

| 3 | $3,600 | $1,440 | $2,160 |

| 4 | $2,160 | $864 | $1,296 |

| 5 | Adjusted | $296 | $1,000 |

Note: In the final year, depreciation is adjusted to ensure the asset reaches its salvage value.

Key Features of the DDB Method

- Accelerated depreciation in early years

- Reduces taxable income faster

- Reflects real asset usage patterns

- Commonly used for technology and machinery

Advantages

Faster Tax Benefits

Businesses can reduce taxable income earlier.

Realistic Asset Valuation

Assets often lose value quickly at the beginning.

Better Matching Principle

Matches higher expenses with higher productivity years.

Disadvantages

More Complex Calculations

Requires year-by-year adjustments.

Lower Profits Initially

Higher expenses reduce early reported profits.

Not Suitable for All Assets

Not ideal for assets that depreciate evenly.

When Should You Use This Method?

The double declining balance method calculation is ideal when:

- Assets lose value quickly (e.g., computers, vehicles)

- You want early tax deductions

- Maintenance costs increase over time

DDB vs. Straight-Line Method

| Feature | DDB Method | Straight-Line Method |

|---|---|---|

| Depreciation Speed | Faster | Even |

| Complexity | Higher | Lower |

| Tax Benefit | Early | Spread Out |

| Best For | Tech, machinery | Buildings, furniture |

Practical Tips for Businesses

- Always consider tax regulations before choosing depreciation methods

- Use accounting software to automate calculations

- Review asset performance regularly

- Ensure compliance with financial reporting standards

Conclusion

The double declining balance method calculation is a powerful tool for businesses looking to accelerate depreciation and optimize financial planning. While it requires more effort than simpler methods, the benefits—especially in tax savings and realistic asset valuation—make it worthwhile.

At The Daily Business, we recommend carefully evaluating your asset types and financial goals before choosing this method. When used correctly, it can significantly improve your accounting strategy.